Clients of mine last week were deciding whether to:

- buy a 1.5 million house in Chatswood (Sydney) to live in; or

- buy 2 x $750,000 investment properties, and rent a 1.5 million house instead (this is the now popular strategy of “rentvesting”)

I’ve reproduced a hypothetical scenario in this article, and this is what the numbers show:

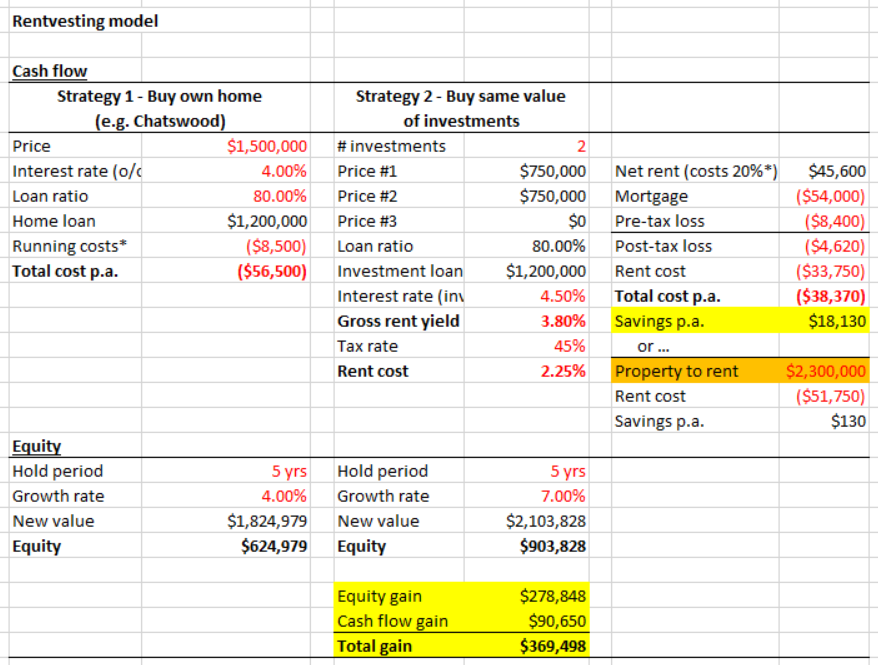

- The rentvesting option (option ‘b’) was $18,130 cheaper to run each year

- This is mainly due to the rental arbitrage of being able to earn rent on your investment properties at a higher rate (say gross rental income 3.8% p.a., what you could potentially earn in a market like Adelaide or Brisbane), but then rent yourself in Melbourne or Sydney where the yields are currently lower (say rental cost only 2.25% p.a., according to Performance Property Advisory’s 2017 E1 research report Sydney’s median rental yield of a three-bedroom house is currently only 2.24%)

- This equates to cash flow savings of 18,130 x 5 = $90,650 over 5 years, despite a) still living, albeit renting, in the same $1.5 million house in Chatswood, and b) still owning $1.5 million worth of property, albeit 2 x investment properties rather than a single owner occupied property

- The clients could instead live in an $800,000 more expensive home, (one worth $2.3 million instead of $1.5 million), still own the same amount of property, and not have their outgoings any higher.

- This is where the title “Would you live in a $800,000 better home, for free” comes from; and

- If the 2 x investment properties grew at 7.0% p.a., but the Chatswood home only grew at 4.0% p.a., then over 5 years they would miss out on an extra $279,000 capital growth

- This would mean the rentvesting option (option ‘b’) could achieve 279k + 91k = 370k more in total returns over the 5 year period

- Whether or not Chatswood does actually return 4.0% p.a. compounded growth, and/or the investments achieve 7.0% p.a. growth, is obviously a critical factor… and no one can be sure of this.

- With parts of Melbourne and Sydney having grown strongly over the past 5 years though, and with all mainstream research suggesting that affordability in both cities is lower in those capital cities now, there may be unrealistic expectations about the growth in parts of Melbourne and Sydney over the next 5 years

- This is the domain of property experts and economists (not lending advisors), but the idea that other capital city markets may outperform over the next 5 years is not unreasonable.

Below is a copy of the financial model which also shows the various assumptions that have been made.

Note that the model assumes interest only repayments and end interest rates reflective of average discounts we’re seeing in the market at the moment.

Remember these assumptions are purely hypothetical and the model should not be acted upon or considered as advice.

I would recommend discussing and stress testing the numbers with professional advisers so you can understand how they relate to your own personal situations specifically.

* Assumed costs for standard items like council rates, insurance, maintenance, water (and property management in the case of the investments)

Australia’s most famous rentvester is Chris Gray from Your Property Empire and Sky News Business – you can listen to my interview with him here.

Keep in mind that the main downside with renting is that the landlord can vacate you from the property, and you can’t simply decorate or renovate the property as you like.

Also as I’ve said before property strategies aren’t only about what’s right or wrong financially, there are also very valid emotional considerations which can be important too. It ultimately comes down to a personal decision and what is right for ‘you’.

Assuming you could pull it off though… renting a $2.3 million house for the same price as buying a $1.5 million house, but still owning the same amount of property… it is an idea worth thinking about.

Question: Which option would you choose?