For most Australian investors over the past three decades, residential property has felt almost infallible. Buy well, hold patiently, apply sensible leverage, and let time do the heavy lifting.

This model has been deeply ingrained, particularly in markets like Melbourne where long-term population growth, limited inner-city land, and growing wealth and incomes have historically worked in investors’ favour.

But it’s a fair question to ask in 2026: has residential real estate, at least in Melbourne, become a dud investment?

Holding costs are now front and centre

It’s not uncommon for me to see relatively modest residential investment properties in Melbourne costing clients upwards of $50,000 p.a. pre-tax to hold.

More expensive homes particularly those with higher land content and/ or more aggressive leverage can cost clients even more.

At the same time, Melbourne house prices have been broadly stagnant for many years. Unlike other capital city markets, there has been little to no capital growth to justify the costs of holding.

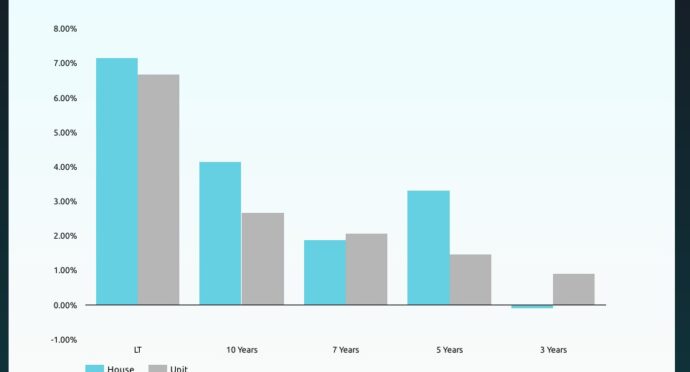

Take a look at the below chart from the research team at Performance Property Advisory…

Despite a long term average growth rate at 7% p.a., it shows house price growth in Melbourne has been negative on average over the past 3 years, and less than 2% p.a. over the past 7 years…

Source: Performance Property, Melbourne research report Feb 2026

On a purely recent-history basis, the argument against residential property in Melbourne looks compelling.

High holding costs, rising land tax, minimal capital appreciation, and now also increasing risk around future taxation, downside risks posed by AI, the Iran war… it is all very scary!!

If you stopped the analysis here it would be hard to invest.

But it’s not all bad news

Consider some of the positives…

- The after-tax costs holding could be nearly halved for high income earners via negative gearing

- The property may have strategic value in that the owners (or their children, or relatives) may move into property at some stage

- The growth rates required to ‘break-even’ aren’t particularly high, for example a $1.0 million investment property costing $25,000 p.a. after-tax only needs to appreciate by 2.5% p.a. to break even

Relative performance against other cities matter, and Melbourne has been the laggard

Over the past cycle:

- Sydney has delivered strong price growth, underpinned by global demand, high incomes, and severe land constraints.

- Brisbane benefited from interstate migration, affordability arbitrage, and infrastructure spending.

- Perth rebounded sharply on the back of commodity strength, rental shortages, and years of prior underperformance.

Melbourne, by contrast, has:

- Carried heavier land tax and regulatory burdens

- Suffered sentiment damage post-COVID

- Seen investors and developers reduce exposure (exacerbating supply shortages)

In a sense Melbourne has already suffered.

Counter-cyclical investing is never comfortable

The paradox a lot of investors naturally struggle with is that investments often feel the least attractive right before they become attractive again.

This is precisely why capital has flowed elsewhere.

Yet the fundamentals that historically mattered most for long-term investment performance in Melbourne remain intact:

- Population growth is strong and structurally supported by migration

- Inner-city land is fixed, no new land supply is being created where people want to live

- Infrastructure, employment density, and lifestyle amenity remain world-class

- Relative pricing versus other capitals now looks compelling

So from a counter-cyclical perspective, Melbourne increasingly resembles a market that has already absorbed its bad news and may now be poised for growth.

Does growth look promising in the medium term?

Investing is forwards not backwards looking.

The real question is whether residential property in Melbourne now looks promising over the next 5 – 7 years.

If Melbourne re-enters a growth phase:

- Break-even growth rates could more easily be met

- Even moderate annual price growth can compound meaningfully over time

- Capital appreciation on quality land can quickly dwarf several years of negative holding costs

- Relative undervaluation versus Sydney and Brisbane can close faster than expected

So… Is Melbourne residential property a dud investment?

The honest answer is it depends on your timeframe, tolerance for volatility, surplus cash-flow and balance sheet strength.

If you have low income and a weaker balance sheet (e.g. no buffer or savings), then residential property in Melbourne may not be the right choice for investment.

On the other hand if you have high income and savings, and you can take a longer term approach, then Melbourne may start looking attractive.

In the right circumstances Melbourne is offering buyers relative value now, and opportunity.

Thanks as always for reading.

—

The Long Property Blog provides general information only and has been prepared without taking into account your objectives, financial situation or needs. We recommend that you consider whether it is appropriate for your circumstances and your full financial situation will need to be reviewed prior to acceptance of any offer or product. Nothing in this article or the Long Property Blog constitutes legal, tax or financial advice and you should always seek professional advice in relation to your individual circumstances