In the last week two LP readers have asked for advice around buying new homes to live in. One was in Sydney, the other was in Melbourne.

They both asked for feedback about the properties they were interested in buying, and their associated strategies.

The Melbourne property was a large 3 bedroom apartment in the prestigious suburb of Armadale. The Sydney property was a modern 2 bedroom apartment with lifts/pool/gym/view in Surry Hills.

Surry Hills and Armadale are both high-value suburbs 2-7km from their respective CBDs. Both properties were expected to be selling for about $1,000,000 (the median price points for the respective property types in each location).

In both cases we provided direct feedback however to introduce the concept of “rentvesting” we thought of outlining some relevant considerations in this article as well.

Introducing rental arbitrage (or “rentvesting”)

Why would you buy your own home which costs $60,000/yr to own (e.g. say a $1,000,000 home with 4.5% interest only mortgage repayments plus 1.5% holding costs, 6.0% on $1M = $60,000/yr), when you could live in the exact same home and pay only $30,000/yr rent (e.g. rental yield of 3.0% paid to the landlord)?

(note the 1.5% ‘holding costs’ above include strata fees/body corporate, repairs/maintenance, council costs and water rates. Mortgage repayments based on an interest rate of say 4.5% are separate).

On face value the ‘buy your own home option’ doesn’t sound sensible, but there are two logical reasons why someone might do this:

- They think it’s a great investment, so the rise in value will make up for the additional cost; and/or

- They want to live in their own home, rather than renting, for emotional reasons

Of course there are other reasons as well — perhaps they don’t know that buying is more expensive, or perhaps they don’t realise that more attractive investment opportunities might exist elsewhere.

Nevertheless the mindset of many Australians is that it’s better to buy than rent. It’s a way of thinking which has been passed down from parents and grandparents who have long aspired towards owning their own home.

If buying and renting costs were the same (or buying was cheaper), then obviously more people would choose to buy, because all else equal, you would rather live in your own home. But all else is not equal.

Mid way through 2016, in the inner-city suburbs around Melbourne and Sydney now, this is far from reality. In fact it’s in these areas now where the cost differential between renting and buying is the highest nationally.

The main reason for this is that over the past few years house prices in inner-city Melbourne and Sydney have increased substantially, and rents have not kept up. So it’s very expensive to buy in these areas now, and the rental yields are much lower than they have been in the past.

But for lifestyle reasons these areas are still highly desirable to live in. There is a lot of demand because being close to the top cafes, restaurants, schools and employment centres is very appealing.

Rent money is only dead money if you don’t invest what you save

Rather than having to settle for smaller or older properties, or buy further away from the city, there’s a growing trend towards renting instead of buying, and then using the money saved to buy an investment property.

This allows people to rent where they want to live, and then buy where the prices may be more affordable, and wherever the return prospects are highest.

This is the idea of rental arbitrage, or “rentvesting”.

To illustrate how significant the buy versus rentvest decision can be, let’s play out the two scenarios for our Melbourne reader, we’ll call him Chris. In scenario #1 we’ll assume that Chris buys the $1,000,000 Armadale apartment, and in scenario #2 we’ll assume that Chris decides to rent in Armadale and buy an investment property in Brisbane instead.

Scenario #1 – Buy owner occupied home in Armadale

For the following reasons many property experts are concerned about short-term price growth in Melbourne:

- following the strong price growth experienced over the past 3 years, prices are now expensive;

- the apartment market is in significant oversupply;

- low yields deter investors and first homebuyers from entering the market (and will in certain cases lead to forced selling);

- much demand over the past 3yrs has come from foreign investors, but the banks are now restricting foreign lending

Nevertheless Chris proceeds with the purchase and in light of the above let’s say his apartment achieves annual growth of only 2.0% p.a. over next 4 years.

Scenario #2 – Rent in Armadale / Buy investment property in Brisbane

In this scenario, instead of buying the Armadale apartment for $1,000,000, Chris decides to rent an identical apartment next door in Armadale, and buy an investment property in Brisbane instead.

From an investment standpoint Brisbane is the market of choice because it’s earlier in its property cycle than Melbourne. It’s more affordable and the rental returns are higher. It’s also underpinned by strong employment, population and infrastructure growth which are key growth drivers.

(Note that Chris rarely travels to Brisbane so a trusted buyers advocate charges 3% to select the best asset and coordinate the purchase).

The property selected is a waterfront property in the blue-chip investment grade suburb of Hamilton, which is 6km from the Brisbane CBD. The property has a large land component and there is potential to add value by opening up the living area and renovating the bathroom. The land is also large enough to one day consider a subdivision and 2-unit townhouse development for additional growth.

The rental cost for Chris in Armadale is $600/wk (again the median rent for a 3 bedroom Armadale apartment), and we will assume that the Brisbane property grows at 8% p.a. over the next 4 years.

Over the last 40 years the long term growth trend in Brisbane has been over 8% p.a. so this assumption is not unrealistic.

Comparing the outcomes

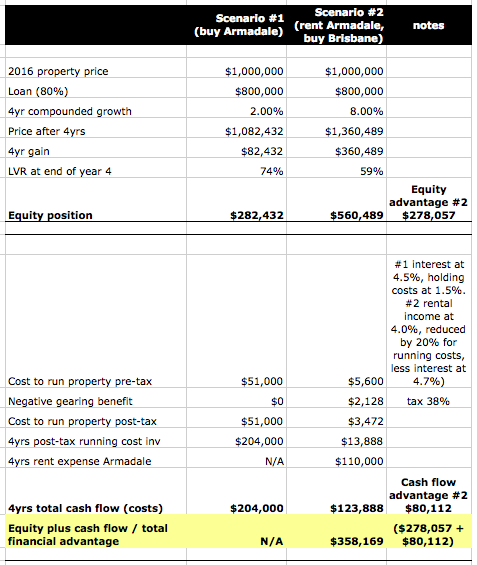

The below table compares the outcomes for Chris in both scenarios:

After 4 years, Chris in scenario #2, the rentvester, has $800,000 owing against a property worth $1,360,489 (LVR 59%). His equity position is $560,489.

Chris in scenario #1 also has $800,000 owing but only against a property worth $1,082,432 (LVR 74%). His equity position is $282,432.

If Chris bought Armadale (Scenario #1) it would have cost him $51,000/yr to run the asset (e.g. 4.5% p.a. in mortgage repayments and 1.5% p.a. in holding costs). But because renting is so much cheaper, assuming a rental yield of 2.75% it only costs Chris $27,500/yr to rent the identical property next door (Scenario #2).

Chris in scenario #2’s Brisbane investment property is slightly negatively geared, so it costs him $5,600/yr to run the asset (e.g. 4.7% p.a. mortgage repayments on his $800,000/80% investment loan = $37,600, less 4.0% rental income discounted by 20% for running costs such as insurance, land tax, property management, maintenance, council rates and water = $32,000).

$37,600 – $32,000 = $5,600/yr running costs for Brisbane.

Chris gets a tax refund of $2,128/yr from the ATO and so the after-tax running cost of that asset is only $3,472/yr or $13,888 over the 4 years.

Over the 4yrs Chris in Scenario #2 pays rent in Armadale of $27,500 x 4 = $110,000, plus the $13,888 running cost of Brisbane, which equals total cash outflow of $110,000 + $13,888 = $123,888.

But this compares to holding costs in Scenario #1 of $51,000 x 4 = $204,000.

So Chris in Scenario #2 is $204,000 – $123,888 = $80,112 better off after the 4yrs in terms of cash flow.

In just 4 years Chris the rentvestor in Scenario #2 is ahead by $560,489 – 282,432 (equity advantage in Scenario #2) + $80,112 (cash flow advantage in Scenario #2) = $358,169 (total advantage).

Final thoughts

Not only can rentvesting be the more attractive financial option, it is increasingly becoming the more practical option as well. This is because many younger Australians are traveling and changing jobs more often, so they’re not ready to settle down for the long term as quickly, particularly if they’re not yet married and/or don’t have kids.

What if the next stage for Chris involved an upgrade to a larger/family home?

If we assume this larger/family home was to be purchased (rather than rented), then Chris’ stronger equity position from scenario #2 gives him many more options.

Essentially he could buy the next property with significantly less cash and/or by taking on less non tax deductible debt (e.g. by selling Brisbane or using the equity from it).

One argument against rentvesting is that you have to pay capital gains tax when you sell investment properties. This is true however the rentvestor doesn’t necessarily have to sell when they purchase their next property. Whereas without any new cash Chris from scenario #1 would be reliant on the sale of Armadale for funding.

Of course renting does have its disadvantages, for example landlord permission is required to make any substantial changes to the property, and there is also the risk of being vacated if your landlord were to decide to sell.

However the ultimate consideration for most people is the trade off between living in their own home (a very emotional decision), versus renting where they want to live, and then investing where they’re likely to be better off financially (a more financial decision).

Those who stand to gain the most financially are those who are comfortable renting and willing to consider investment opportunities wherever the return prospects are highest.

Perhaps Australia’s most well known rentvester is Chris Gray from Sky News Business and Your Property Empire. Chris spoke to Long Property about rentvesting and you can listen to the recording here (start playback at 19:36).

What are your thoughts on rentvesting? Do you agree with the financial advantage and do you think this is worth the trade off of not living in a place that’s actually yours?