Welcome back and best wishes to all readers for the new year.

In an article I wrote last November I discussed the investment rationale for buying in the blue chip suburbs surrounding Adelaide CBD. (see here)

As a continuation of that article I am now providing a detailed case study of a property my wife and I recently purchased in Adelaide. I’d be keen to hear your thoughts.

Consider this in the context of what else you could do with your next property purchase. E.g. you could buy local or interstate, you could buy a home to live in or an investment property.

What’s right for you… the emotional, or the financial?

By way of background this was our strategy:

- Target maximum short term growth 2-4yrs

- Budget $700,000

- Gross rental yield 4.0% p.a.

- Buffer in place to run cash loss

- Trust ownership for asset protection and to utilise tax loss

Investment criteria agreed with our buyers advocate:

- Budget and target yield as above

- Blue chip suburb within 5km Adelaide CBD

- Double fronted bluestone/sandstone period style cottage

- Opportunity to add value through renovation or development

- Immediately rentable or with minimal works

- Bought at or below fair market value (preferably an “off market” purchase)

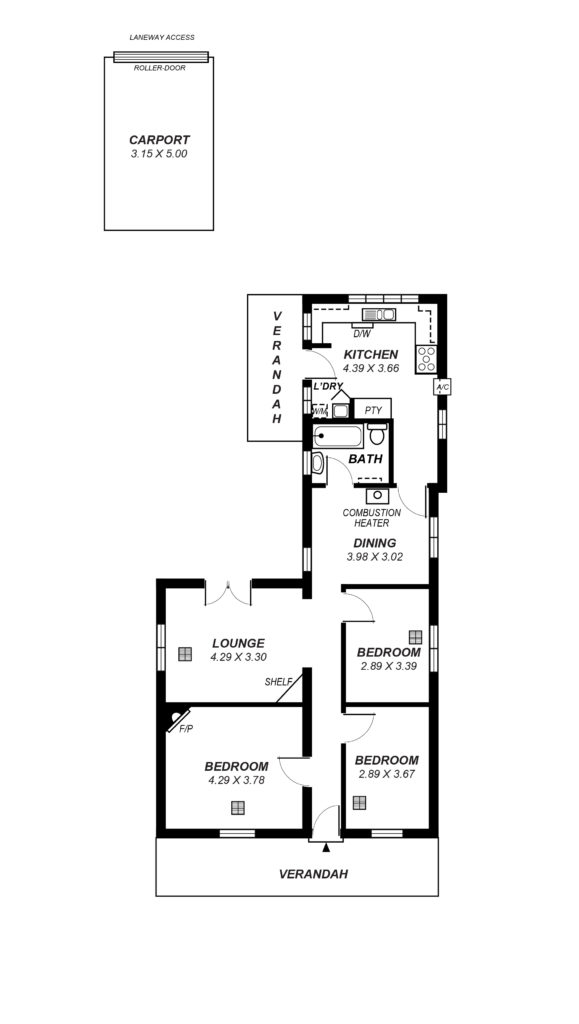

Over the course of several weeks our buyers advocate presented a number of properties to us, but the one we eventually purchased was this property in Eastwood, South Australia (2.5km from Adelaide CBD).

Our buyers advocate went through the property on a Wednesday, we reviewed his investment report that afternoon and then conducted further research ourselves. Following a 72hr negotiation process signed contracts were exchanged by Saturday and we owned the property 30 days later (we offered a shorter settlement term to negotiate a lower price). After some minor touch ups it was immediately rented for $520/wk (our asking price) after the first inspection, this represents a gross yield of 4.05%.

It was an off-market (“silent sale”) transaction, so the property was never listed on realestate.com.au and there were no other interested buyers that we had to compete against. The vendor was moving back to Melbourne and had already purchased a new home there, she had contacted her real estate agent (who knew our buyers advocate) and was happy to proceed with a quick sale.

The property was purchased for $667,500 which was below our budget and well below what our buyers advocate believed the property was worth (estimated true value approx. $725,000).

This is one of the (many) key reasons for using a buyers advocate, getting access to off-market deals which enable you to purchase properties at or below their fair market values. The likelihood of overpaying increases when there are more buyers you have to compete with, this can be very apparent in auction scenarios.

Here are further details on the purchase.

Subject property:

- Purchase price $667,500 in Sept 2016

- Suburb: Eastwood, SA (shares 5063 postcode with Parkside)

- Proximity to Adelaide GPO: 3km south east

- Building and car accommodation: 3 bedroom, 1 bath, 1 single carport

- Year built: c.1880

- Style: Double fronted, single storey, detached

- Main walls & roof: Bluestone, brick, corrugated iron roof

- Land: 334sqm (on 2 x titles, 167sqm each title)

- Site: Regular shaped flat allotment

- Additional feature(s): Rear vehicle access, block on 2 titles (finding a site on 2 titles presents major upside by way of development potential, more on this below)

- Refurbishment type & budget: Cosmetic/$20,000

- Rent $520/wk (gross yield 4.05%), rented at asking price after first inspection.

The following comparable sales suggest the property was purchased for at least $50,000 below market value.

10 Markey Street, Eastwood SA (link to realestate.com.au listing)

- Comparable location (500m from subject)

- Inferior accommodation (single fronted 3bd/2bth cottage, semi renovated)

- Inferior land area (185sqm vs. 344sqm)

- Overall: Inferior

- Sold for $665,000 on 17th December 2016

5 Elizabeth Street, Eastwood SA (link to realestate.com.au listing)

- Comparable location (500m from subject)

- Inferior accommodation (single fronted 3bd/1bth cottage, semi renovated)

- Superior land area (536sqm vs. 344sqm)

- Overall: Superior

- Sold for $835,000 on 28th January 2017

41 Jaffrey Street, Parkside SA (link to realestate.com.au listing)

- Comparable location (750m from subject)

- Inferior accommodation (sandstone 3bd/1bth cottage, semi renovated, only single fronted)

- Inferior land size (266sqm vs. 344sqm)

- Overall: Inferior

- Sold for $692,000 on 22th October 2016

Also see:

21 Dunks Street, Parkside SA (here)

- Slightly superior (366sqm, also double fronted), sold for $760,000 on 4th July 2016

31 Jaffrey Street, Parkside SA (here)

- Inferior (only 224sqm, single fronted), sold for $675,000 on 8th October 2016

17 Liston Street, Parkside SA (here)

- Slightly superior (larger block 426sqm), sold for $756,000 on 5th November 2016

The last sale for our subject property in Eastwood was $375k in 2004. We successfully purchased the property for $667,500 in September 2016.

Renovation potential

In terms of being able to add value to the property, one option is to remodel the back section of the property and convert it into a more open and free flowing floor plan, commensurate with what most buyers in the market today are actually looking for.

With this modification the property could reasonably fetch ~$900,000 once renovated, see precedent here:

13 Anglo Ave, Parkside SA (link to realestate.com.au listing)

- 487sqm, 3bd/1bth double fronted – renovated

- Sale price: Sold for $875,000 on 24th October 2015

Development potential

But what’s particularly interesting about the property is that it’s on 2 separate titles (e.g. the land is divided right down the middle into two separate lots).

What this means is that instead of the renovation above, the double fronted cottage could be converted into 2 x single fronted cottages (e.g. one on each lot), both with rear lane access/car spaces. The upside here is potentially much greater.

The dwelling is heritage listed so the development would involve retaining the façade and front four rooms of the house, and then redeveloping the back of the house, and also building a second story.

A dividing wall would separate the two dwellings and a new entrance would be built for access into the LHS property.

So the single 3 bd / 1 bth / 1 car house would be converted into 2 x 3 bd / 2 bth / 1 car double storey houses. Here is a 3D render of what the finished product might look like:

The economics would like something like this (figures are still estimates at this stage):

Costs:

- $667,500 purchase

- $20,000 consultants and development approval

- $20,000 renovation (to increase rent prior to development starting)

- $400,000 construction

- $20,000 holding costs

- $1,127,500 total acquisition and development costs

End values:

- $800,000 semi detached cottage #1

- $800,000 semi detached cottage #2

- $1,600,000 total value

Profit 1.6 million less 1,127,500 costs = $472,500 (assuming 0% capital growth from purchase to the end of the development)

Comparable sales of new SA developments to justify end values $800,000 are as follows:

- 7/165 Beulah Rd, Norwood SA – 3bd / 2 bth, sold for $985,000 in Dec 2016 (link to realestate.com.au listing)

- 2 Bruce St, Frewville SA – 3bd / 2 bth, sold for $825,000 on 29 Nov 2016 (link to realestate.com.au listing)

- 58/220 Greenhill Rd, Eastwood SA – 3 bd / 2 bth, sold for $770,000 on 8 Aug 2016 (link to realestate.com.au listing)

If Adelaide achieves the short term price growth that many of the experts predict, then the upside is higher again. (refer this article for further details on the outlook for Adelaide)

Having council approve our development application is not certain and the above costs & end values could all easily change. However the development opportunity is still highly lucrative and worth careful consideration.

Property and development summary

In summary, our Eastwood property was bought approximately $50k (~7%) below market value in a major capital city with a strong track record for growth and clearly at a low point in its current cycle. (again refer this article for further details/research on the Adelaide housing market)

It’s a relatively inexpensive purchase in a blue chip suburb 2.5km from the CBD. It’s a character home with period features on a good size block in a quiet street. It’s close to cafes/restaurants and public transport, it has high owner occupier appeal and there are numerous opportunities to add value.

The potential development profit is approx. $500k and that’s with zero assumed capital growth.

Strategy in the context of broader short/medium term goals

Our current intention is to pursue the development and hold both properties for at least 3-5yrs. At that point we will either use the equity to buy a larger family home in Melbourne without needing to use any of our own cash, or we may decide to sell both assets and then buy the Melbourne home with a significantly lower (non tax deductible) home loan debt.

Ideally this occurs once the Melbourne market has cooled and the new home can be purchased in what becomes a more buyer friendly market (Melbourne is currently a sellers market).

Aren’t we better off buying a $1.5 million house in Melbourne?

The more emotional decision would be to buy the dream Melbourne home for $1.5 million today – we could easily afford this, and any bank would be only too happy to lend us the money.

But this property in Melbourne is currently renting on a 2.5% yield only (yields in Melbourne and Sydney at the moment are very low), the landlord is only receiving 1.5 mil x 0.025 / 52 = $720 per week rent.

So by moving into the same $1.5 million home as a tenant (instead of buying it), just on the rent vs. mortgage repayments alone we would save $205/wk (e.g. $720/wk rent vs. interest repayments of $925/wk assuming an 80% lend on $1.5 million at 4.25% interest).

These savings of $10,660 p.a. (e.g. $205/wk x 52) can go towards the Adelaide investment, or alternatively towards building up a larger cash position.

And instead of having to come up with $386k to cover the balance of the Melbourne purchase (e.g. 20%, or $300k), plus purchase costs (e.g. stamp duty/registration etc., $86k), we only needed $169k cash ($217k less) to buy the Adelaide investment property.

The other risk of buying today in Melbourne is that if the property experts are right and the Melbourne market flatlines for 3-4yrs, then we would have to endure 3-4yrs of no growth, and then potentially be left with a much larger home loan. (please contact me if you would like me to send you up to date research on the price forecasts for Melbourne).

So we would much rather buy the same house in Melbourne in 3-4yrs time, and hopefully buy it at the same price as it is currently selling for today (e.g. $1.5 million or $1.55m in 3-4yrs, assuming the market does flatline). With the right structures in place we could do this either without having to contribute any cash, or with a much smaller home loan debt.

And lastly, it is worth pointing out that as a young couple our circumstances today are very different to what they’re likely to be in 3-4yrs time. Right now we have to be in close proximity to the city, but in 3-4yrs it’s likely that we’ll have kids and need more space, even if that means having to pay more or move further away from the city.

So if it turns out that the $1.5 million dollar dream house today is not the house that we actually need in 3-4yrs time, then we won’t have to sell and re-buy, in which case we would end up wasting $86k stamp duty on the way in today, plus approx. $30 selling costs on the way out in 3-4yrs time, and then another $86k stamp duty to buy the second property after that. (total transaction costs $202k).

Not only does the investment strategy make more financial sense, it also offers a great deal more flexibility.

Balancing financial vs. emotional considerations

One obviously needs to balance the emotional and financial considerations of real estate, but the right financial decision for my wife and I here was clearly to pursue the interstate investment, rather than the Melbourne home purchase.

The relative importance of emotional versus financial decisions is different for everyone, and also changes with time. So what’s right or wrong for you might be totally different for someone else, and it may even be different for you in a few years time. From this perspective there’s no “one right answer”.

Of course I’ll support clients no matter which path they choose to go down. My job is to ensure clients at least understand the various options though, and allow them to make more informed and better educated decisions.

—

(you can re-read my part I article on the Adelaide market here. In March 2017 the bank revalued the Eastwood property at $730,000).

Question of the day: What is more important to you right now, the emotional or financial considerations for your next property purchase?